Are you FI but not MI? Medically Independent, that is. How can there be shockingly simple math to early retirement if no one can estimate their health insurance costs? Having retired years before Obamacare went live, let me tell you our approach to this ever-changing and costly budget item.

Shockingly Simple or Shockingly Complex?

If you’re busy pursuing financial independence, you’ve undoubtedly heard it. Save 25 times your estimated spending and voila, that’s your number. The phrase “shockingly simple” has been made famous by Mr. Money Mustache in his most influential post demonstrating how simple it is to calculate the number of years you need to FIRE, or become Financially Independent and Retire Early.

This 4% rule in itself has been debated in financial circles and many now refer to it as a “rule of thumb” (thanks Big ERN!). In this environment of stock market and real estate highs, it may be better to take a more conservative approach and use a 3% rule as your target for early retirement.

But even then, the big question is this:

How can we estimate our annual expenses if we can’t estimate our health care costs?

In particular, if you are receiving health insurance through your employer, you probably have no idea what it is going to cost when you pick up the tab.

Warning! The Stress of Paying for Health Insurance is not covered by Health Insurance.

The Big Question

Just this weekend, we got news headlines that a judge declared Obamacare unconstitutional. And while this case will need to wind its way through the courts, it serves as a wake-up call that the current system in the USA is rapidly changing.

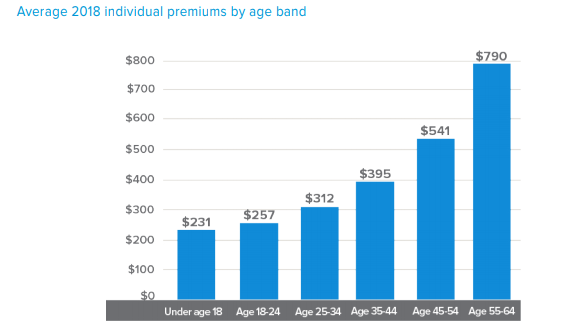

Couple that with the fact that not only are costs and insurance plans changing every year, but they vary widely depending on your age.

For instance, consider this graph from eHealthInsurance Services:

As you try to estimate your future health care costs, it is really important to plan differently for the various decades you plan to be living off of your lifetime savings.

And if you think this problem is solved once you reach Medicare age, think again. For example, I handle the finances for my husband’s 89 year old parents. Their premiums for supplemental insurance and prescription coverage run them about $800 per month. And then on top of that, the out-of-pocket costs for prescriptions cost about $3000 every year. Granted, it depends on how many prescriptions you have, but none of us know how many medications we’ll be taking when we are in our 80’s.

As a quick overview, here are several different parts of the cost:

- Premium – the monthly cost of a plan, paid even if you use zero services that year

- Copays – one time fees for routine doctor and lab visits, which don’t count towards your deductible

- Deductible – the amount you pay first prior to any coinsurance cost sharing

- Coinsurance – then a percentage of the bills paid by you until reaching the maximum out-of-pocket expense

- Maximum Out-of-pocket – copays + deductible + coinsurance max per year (does not include premium)

To dig a little deeper, I would highly recommend you read Health Insurance 101 from Ms. Fiology, who works in the field. In it, she explains the possible ways to obtain insurance (employer, ACA, health sharing ministries, Medicaid and Medicare).

These definitions are only valid for the rules in place today, in 2018. Who knows what rules we will navigate going forward. And the younger you are, the more changes you can expect to see in your lifetime.

I Need a Life Preserver!

We Retired Before the ACA Exchanges

When I first quit my job in 2010, my husband was still working and I was covered by his employer-sponsored health plan. It wasn’t until he retired in 2013 that we had to figure out the puzzle of health insurance.

Two big questions needed to be answered in order to fully FIRE:

- What should part of our net worth do we expect to spend on average, over the rest of our lives on health care expenses?

- What do we expect to spend this first year?

Some people consider using COBRA. I recommend reading how The Groovies chose COBRA prior to Obamacare when they quit in 2016. Or this post from TheFinanceBuff weighing COBRA vs the ACA and health sharing ministries.

One problem with COBRA is that the “better” your insurance coverage is, the higher price you have to pay. This is because you are paying to continue the plan you are on. At that price. This was really important back when preexisting conditions could be excluded from coverage.

We did not have any preexisting medical conditions, and COBRA was going to cost over $1600/month in 2013 dollars for the premium alone.

So we opted to buy our own plan. This was the first time we ventured into the private marketplace. It was a little scary, I have to admit.

We Bought a Catastrophic Plan, But…

We purchased a high-deductible catastrophic plan in 2013. And we liked the plan. But it was eliminated in 2014 when the Obamacare exchanges went into place.

Today, you can only purchase a plan like this if you are under 30 or qualify for a hardship. But these plans might return, especially since the Individual Mandate has been eliminated starting in 2019.

The plan we purchased had a premium of $500 per month for the two of us. That’s $6000 to start with, if we used no services at all. Then, it basically covered nothing at all until we hit our $5000 deductible (per person), and then it paid 100% of the costs. So our costs could run as high as $16,000 if we both maxed out.

I’ve written about how we design our expenses for wild swings so this type of plan suits us. We would rather have low premiums and occasionally a large bill to pay since we have a high net worth to draw from. That plan seemed reasonable at the time. It fit our needs.

We Don’t Want a One-Size-Fits-All Policy!

Since 2014, We Limit Our Income to Get Obamacare Subsidies

One advantage to pursuing FIRE is the combination of high net worth and low spending needs.

The tax law generally favors lower income, regardless of net worth. The Obamacare subsidy is an rare example that not only follows this principle, but is available with a fairly high income.

Available if your Modified Adjusted Gross Income (MAGI) is below 4 times the poverty level, this “line” is quite generous for being eligible or a tax credit. In 2018, that is $48,560 for a single person or $65,840 for a married couple.

A good post at GoCurryCracker covering tax minimization and Obamacare, although written in 2015, is still a very good look at the tax tradeoffs.

Each year since 2014, we have used the Covered California exchange to search for and choose the plan that best optimizes our particular situation. We originally projected our spending level to be $70,000 per year. Of that, we thought that we might pay around 20K of that on health care.

But we have received a very large subsidy each year by keeping our MAGI below the 4X poverty line. This coming year for example, we will receive about $20,000 in subsidies and have a premium of $125 per month covering the two of us. That plan is a Gold Coinsurance plan with Kaiser. It has zero deductible, but a whopping $7200 per person out-of-pocket maximum.

We have chosen Bronze plans most years, which are the closest to the high-deductible catastrophic insurance we prefer. That’s just us. As rare medical users, with no prescriptions, we rarely go into see a doctor, so it makes sense to keep our premium low and roll the dice, so to speak.

We like to Play With FIRE, right?

Our Upcoming Problem — Massive IRA RMDs

There is just one problem with limiting our income. We are not doing any Roth conversions. A large portion of our net worth is tied up in IRA accounts and the tax bill is like a time bomb ticking away.

When we reach the age of 70.5, we will have Required Minimum Distributions (RMDs), which will force us to start withdrawing 3.6% and more each year from our accounts. Here is a table from the IRS that shows how much you have to withdraw year by year.

For us, my husband is 62 and I’m now 59. Assuming I continue on Obamacare until age 65, that will only leave us two years to get money moved over. Once we hit the RMD age, the law only allows the amount over that RMD to be converted to a Roth.

The new tax law makes it even more tempting to convert now rather than wait. The 24% tax bracket for a married couple goes all the up to $315,000. But as California residents, we would pay 10.3% on that extra money. Couple that with the loss of $20,000 in Obamacare subsidies, we have decided not to convert any time soon. We most likely will move out of the state when the time comes.

So for now, we are keeping our income under the “line” and taking the subsidy.

I See a Bright Future! Don’t You?

What About the Future?

It is so hard to predict the future. Everyone tells us we can’t forecast the stock market. No one has a crystal ball. And yet, we are supposed to retire early not being able to guess what we are going to pay for health care in our future.

What should we do? What did we do?

Honestly, for us, we did two things. First, we are what many call fatFIRE. Count us as examples of people who overshot the goal post. In this post from Fritz at TheRetirementManifesto, he discusses the unknowns of health insurance costs as one of the big factors to consider when picking your target FIRE number.

The second thing we did was to just say “what the heck” and quit anyway. Figure it out later. Not all things are going to be known. As I wrote about in my post about backpacking, it’s all about flexibility and adapting. You can plan and plan, but the reality is that things will change.

This is one of the main reasons I stay engaged in the financial arena and learn from a lot of smart people out there. It is incredibly helpful to see what others are doing to solve these tricky problems.

Follow Me!

What are Other Early Retirees Doing?

Finding out what others are doing can be tricky. For instance, Tanja from OurNextLife has a great post regarding their health insurance decision making. But she also wrote a post warning that famous bloggers are earning money from their websites and may not be a good comparison for you as an early retiree.

That said, here are some posts that I recommend taking a look at to see how others in the FIRE community have tried solving this problem:

- ESI Money explains using Samaritan Health Share Ministry

- ThnkSaveRetire talks about using Liberty Health Share

- MrFr33 shares a story visiting a hospital in Thailand

- RouteToRetire talks about Expat Health Insurance for his move to Panama

- Retirement Manifesto has a post about Health Insurance Unsolved with a spreadsheet showing articles on this topic

Here are some other posts that I found helpful when considering the complex subject of health care costs:

- Michael Dinich on hacking the ACA

- This Bloomberg article talks about people opting to skip buying insurance at all

- Medical Tourism was discussed by Myles Wakeham on this ChooseFI podcast, particularly covering dental costs

- An excellent panel discussion how health affects FI was the topic of this What’s Up Next podcast

- MillenialMoneyMan has an overview of Health Share Ministries

- AccidentalFIRE has a post about the difficulty of making a health insurance claim

And one last thought is simply to try to be healthy and make smart decisions to lower your costs. This post by White Coat Investor has a lot of ideas and recommendations to consider.

Thank you for such a thoughtful and informative post, Susan! I look forward to reading the other articles you linked to as well. Figuring out health insurance is difficult all around. Besides trying to catch up my retirement savings, health insurance is another thing that keeps me at my job for the time being.

I hope these articles help people like you to get this part of the retirement plan estimated better. Finding out what others are doing really helps all of us, especially as you make the plan to leave work. Good luck getting there. I know you are close.

“what the heck” and quit anyway. Figure it out later.

I want to do this, but my risk tolerance just isn’t there. I envy you and others who have the cahones.

Right now I need to stay where I’m at with my employer plan and part time status. To be honest keeping my foot in the working world part time has served me well in many ways. In other ways, not so much. Like everything, ying and yang.

Lastly – you need to post more next year 😉

Having a part time work schedule and getting to be on the employer-sponsored plan is a rare opportunity. Golden handcuffs, no doubt. When the time comes to FIRE, you actually will find yourself saying “What the heck” because there will always be unknowns. It’s sort of like hiking or climbing a big mountain — you can’t see the top or around the next corner, but you have faith in your abilities and know you’re prepared.

Posting? What? I’m a guest poster here 🙂

I agree wholeheartedly that you can plan and plan for healthcare needs, but with the state of things, eventually folks should just consider pulling the trigger and be flexible. The key is that you probably shouldn’t just jump ship until you’ve at least gotten in an area financially where you feel you can handle what you anticipate the costs to be,

The health industry in this country is such a train wreck it just makes me shake my head in disgust.

Awesome post, Susan!

— Jim

PS Thanks for the mention! 🙂

Articles like yours are really helpful. Just before I quit my job, I worked with a guy from England who has a home in Philippines. His stories of getting great hospital care for cheap in places like Thailand really opened my eyes. It gave me a sense that there were alternatives elsewhere if things become too expensive in the USA, and it helped me pull the trigger and quit my job. Your story in Panama will be very useful for people in the FI community to learn from. Thanks for your contribution.

I like the term Medically Independent. I have been trying to figure out the right number for medical costs and it has been difficult. I think I am pretty comfortable with the numbers (especially with ACA subsidies).

My biggest issue is the poor coverage from the marketplace plans in our area. None of the specialists I see are covered, so I am actually thinking of going self-insured when I need to see them (it is just standard lab work). This would definitely put us closer to the FatFIRE bucket.

I keep trying to get to the mindset of “what the heck, figure it out later.” The more research I do on coverage options the closer I get to that point.

Thanks for writing this informative piece.

I really appreciated hearing you and Dragon Gal on the What’s Up Next podcast. Your case is particularly difficult since you deal with a chronic condition and have specific doctors and hospitals you wish to continue with. We all want to stay with our doctors, but we don’t feel the importance of it as you do. Yet we probably should. I’m so impressed that you are able to consider the “figure it out later” mindset. No matter how much we plan, the reality is that we will have to deal with a changing system. I believe if I were in your place I would choose time over money, but it is easier said than done.

MIRE? Too bad we’re all stuck w the reality of a very complex health insurance minefield. Thanks for the shout-out, always interesting to see how others are managing this frustrating reality of early retirement!

Yes, we are all MIRE’d in the difficulty of this confusing and changing system. Your post is really helpful in sorting out this subject. I plan to continue gathering links like you are to help figure this out as it evolves. Thanks for your input!

We have a bout 10 to 15 years before we retire, and we plan on as fat as we can. FIRE is really about a plan B for us, and this whole plan is about giving us more options in any fincancial sitation. I have wondered a lot about health insurance, and what to do in the future. I guess we will have a lot of time to watch how others like you deal with it, so I can say thank you.

To put some personal spin on this, it has kept me up a bit. Those costs are why we we want a fat FIRE instead of a more leaner option.

I suspect that the entire system will be different 10 to 15 years from now. It may also be different for employer-based plans too. I think going for a fatFIRE is good if you can swing it. Not only because of health care, but it makes weeks like this last one in the market easier to handle. And that helps keep the stress low, which is the real key to healthy living!

Well, that’s the whole thing. FIRE is about giving you options. FAT gives you more. That’s the whole movement to me. My parents were quite poor, and my wife’s were as well. We are definitely reacting to their stories

Thank you, Susan, for mentioning my article.

Wow, those COBRA rates are high! And that was in 2013 dollars.

I like your strategy of overshooting the FI mark and additionally just saying what the heck. None of us has a crystal ball and that includes healthcare. We plan & adapt.

Happy New Years to you & yours!

Your article is one of the best overviews that I’ve found. It helped me to learn which parts we pay go toward the out-of-pocket max. I love the resources that are shared in our community and with you being a professional in the field, it is a true gift for all of us. Yes, in the end, we have to plan and adapt. That is really what keeps us all healthy. Thanks for your contribution here and Happy New Year to you as well.

Health Insurance is even worse here in Canada. Everyone thinks because it’s “free” that its the best thing ever. Well let me tell you it’s not, huge waiting times, lack of doctors, some drugs/ procedures not being covered its really a mess. Then if you retire without your own plan its a totally different ball game. Anyone know of a country that actually has figured out how to run health insurance correctly?

That’s quite interesting, sadly. I personally was working in Scotland on and off during my last job. Due to long hours and lack of food on a crazy Oil and Gas project, I ended up in the Emergency Room with symptoms of a heart attack. The “free” health system went into action after hours and hours of waiting. They took my blood pressure and sent me on my way. Since my project was going through thousands of dollars a day, I insisted on getting an EKG, which they provided me through a private clinic used by workers going offshore. The facility was amazingly modern and I got the testing I needed to assure that I was not in danger and could travel home without risk. As I spoke to my coworkers from Scotland, they said that there was a 2 tier system and that the “free” health care provided very little. As I boarded my flight home, in March of 2009, I saw a headline on the television that Obamacare had just passed into law in the USA.

I am not saying I know the answers to any of this. We all just know that health care is a huge unknown and that a “free” system will not solve that problem either. Thank you for your comment and contribution to the discussion.

Thanks for such a comprehensive reference on one of the biggest challenges (and headaches) of formulating a FIRE plan. As I also commented on Retirement Manifesto, I am using COBRA for my first 18 months of early retirement (which started last June). With our income last year and likely this year (my wife is still working for the time being), we’d fall off the subsidy cliff in an ACA plan. After this year, we’ll reevaluate our options depending on whether my wife is still employed.

The uncertainty around medical costs and the future of health insurance in America introduces an uncomfortable amount of voodoo estimation into expense planning. Possible long term care events are also important to consider. However, like you, we are fat FIRE, so we felt comfortable with taking the leap of faith and jumping into the fire.

It looks like you are early retired just about the age I started and you are living not too far away, so our situations are quite similar. I can see why you took COBRA since you are above that cliff for now. My experience is that the ACA line in the sand does affect almost all of our income planning. In a way, it is one of the reasons I’m currently drawn to the FI community. People are great at sharing ideas and hacks that will allow you to live off of less money, like Travel Rewards for instance. Using many of these tips and extra time to thrift shop, etc, allows us to live really nicely in spite of that. It’s great to hear from you and I hope to meet up sometime soon.

My wife still works so it’s not a problem for us right now. We’ll have to figure it out when she retires in a few years. We’ll probably get a silver plan from Healthcare.gov. The RMD will become a big problem for us too. We have a lot of money stashed in the traditional IRA. We still have lots of time left to figure it out so I’m not worried too much about RMD. Maybe we’ll go live in Thailand for 5-6 years. That way we can withdraw some money from the IRA without having to worry about the medical care subsidy.

Living in Thailand for 5-6 years would definitely save on health care. You might be able to limit your taxes too if you’re willing to stay out of the USA for the official number of days. It is so nice to have options, that is the main thing. Good to hear from you and welcome back!

As someone who has had health problems since age 19, I always worry about FIRE folks underestimating how expensive it is to be sick. I’m glad to know that there are more people than I thought who are crunching the numbers — inasmuch as you can plan for this type of thing.

I’m shocked that your in-laws pay so much for supplemental coverage through Medicare. It really shouldn’t be that pricey by any stretch, but maybe the plans are different where they live than from where I do. Either way, it’s nice of you to help them out the way you do.

I just took a look at your blog and your story is both heartbreaking and honest. The preexisting conditions issue is an unknown that affects you very personally as well as all of the costs for copays and deductibles that a person like you factors in much more carefully than others that are currently healthy. My in-laws are 89 now and I have certainly learn a lot seeing first-hand how their costs are coming in. The FI community has not really addressed the old age problems as well because so many are looking to leave work at a young age. Being 59 and having retired at 51, I believe I’m seeing both the perspective of the younger folks and the older, more traditional retired people and their challenges. I truly hope this post helps you in some small way, with the links to others looking to crack this difficult problem. Take care.

Nice write up. It is almost to the point where we should have a completely separate investment portfolio dedicated to future healthcare costs. Listening to the debates, the “future” is getting even harder to predict. Even a ‘Medicare for all’ scenario would likely come with a lot of cost-share like deductibles and co-payments like the traditional program has built-in. It is hard to plan for those when you don’t know what they will be.

Even with a separate investment portfolio earmarked just for health care expenses, we would withdraw from the main portfolio once it depleted. If only you could buy a lifetime medical annuity, just for health expenses. And then what? That insurance company could go belly-up. I tell you, this is a tough nut to crack. It’s sad that many people that have saved enough to retire early are still in the work force just for medical coverage. I truly wish we had better options. You are right, no matter what the options are, you can count on them changing in the “future”. Thanks for your comment.